Stablecoin Supply at All‑Time Highs: What Actually Changes for Business and Fintech

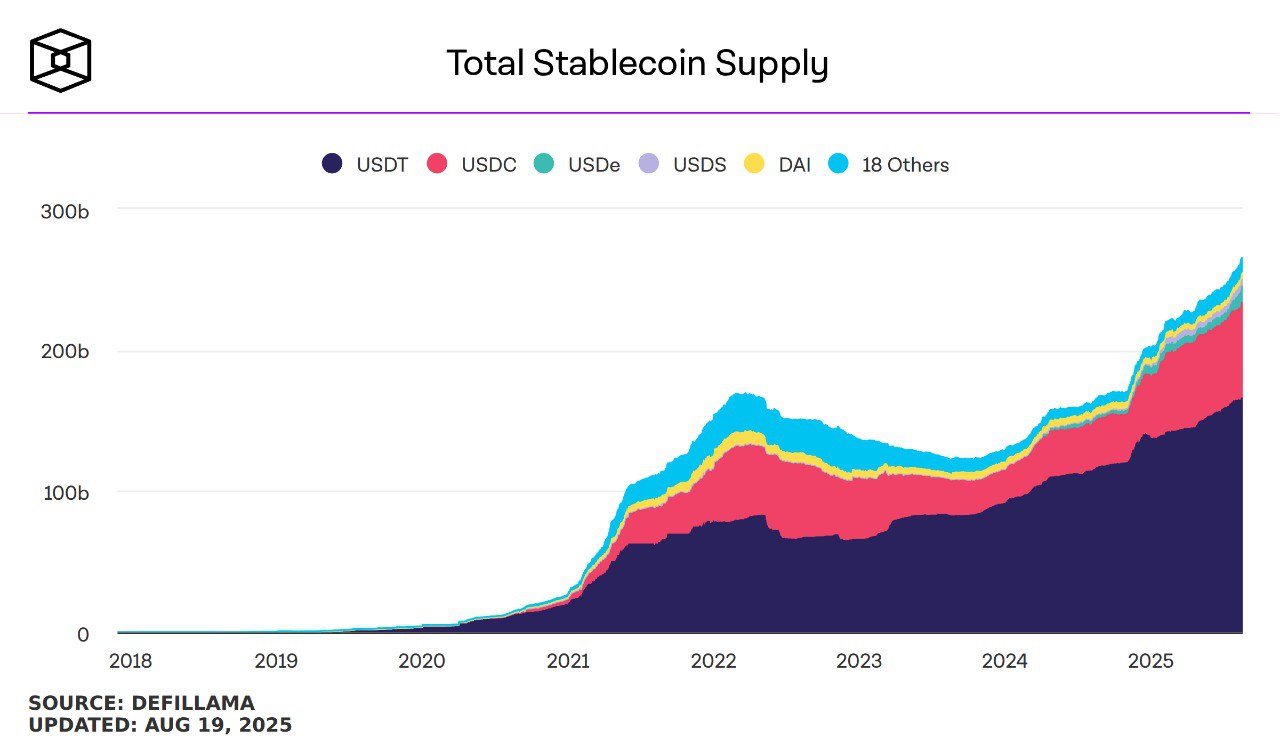

The stablecoin supply hit $160B today, and the implications of what it means go beyond mere liquidity.

Regulatory acceptance (such as the GENIUS Act), major Wall Street firms (and TradFi) integrating stablecoins in their systems, payment providers (and even banks) using stablecoins - all of this lead up to this, which is why stablecoins are on such a rise.

Because of this, it’s important to see what this changes for businesses and the whole fintech field.

We would like to point out the following effects that the record-high stablecoin supply can have:

1) Payment Rails: Lower FX Friction, Faster Settlement, New Cross‑Border Margins

- Growing stablecoin float increases on‑chain USD “inventory” sitting closer to end‑users/merchants, compressing end‑to‑end settlement times from T+2/3 to near‑instant finality in many corridors. This pulls volume from card networks and SWIFT in high‑fee, low‑service markets.

- FX becomes “USD‑as‑a‑service”: SMEs in EMs can invoice/collect in stablecoins, net exposure intra‑day, and convert only at payout, shrinking their effective spread vs. bank wires and marketplace payout rails.

- Merchant acquiring changes shape: processors can price differently when chargeback risk and batching costs drop, enabling sub‑1% take rates on crypto‑native flows where compliance is embedded at the wallet layer.

2) Treasury and Working Capital: On‑Chain Cash as an Operating Asset

- Corporates increasingly hold operational buffers in tokenized dollars to bridge weekends/holidays and move funds between exchanges, PSPs, and banks 24/7. This reduces idle cash and the need for daylight credit.

- Programmable disbursements (payroll, supplier payments, refunds) shift from batch ACH to event‑driven, reducing float requirements and reconciliation breakage.

- Interest transmission changes: if more supply is in yield‑bearing wrappers (sDAI, USDM‑style, tokenized T‑bills), the baseline return on operational cash creeps up toward risk‑free, tightening tolerance for non‑yielding PSP balances.

3) Market Microstructure: Tighter Basis, Deeper Perp Liquidity, Lower Volatility Spikes

- More stablecoin collateral on centralized and on‑chain venues generally tightens funding rates and the spot‑perp basis during stress; liquidations clear faster when quote size and depth are thicker.

- Fiat on‑ramp constraints matter less intra‑crisis when stable USD liquidity already sits on‑venue; this dampens “cash premium” blowouts that historically whipsawed prices during banking or off‑ramp outages.

4) Banking Interface Risk: Reduced Single‑Point Dependence, New Compliance Surface

- After past off‑ramp disruptions, a larger circulating float reduces dependence on any one correspondent bank. Settlement can route stablecoin→stablecoin across venues, with fiat only at edges.

- Compliance moves upstream: wallets, stablecoin issuers, and on‑chain analytics become primary KYC/AML control points. Expect sharper regulatory differentiation between permissionless transfer and permissioned access (whitelists, travel rule messaging, provenance scoring).

5) Remittances and B2B Cross‑Border: Pricing Power Shifts to Front‑Ends

- Consumer apps with stablecoin rails can undercut MTO spreads while offering instant availability and recipient optionality (cash‑out, hold USD, swap to local). The “liquidity moat” moves from bank agents to user distribution and cash‑out networks.

- In B2B, stablecoins become the de facto settlement layer for marketplaces and SaaS billing across multi‑currency contexts, with FX consolidated at treasury rather than per transaction.

6) Tokenized RWAs and Short‑Duration Credit: Cheaper, Continuous Funding

- A larger stablecoin base is natural demand for tokenized T‑bills, repos, and money‑market equivalents. Short‑term funding costs for fintech lenders can fall as they tap on‑chain credit lines collateralized by stablecoins with real‑time margining.

- Expect a steeper differentiation between “pure payment” stablecoins and yield‑bearing/tokenized‑asset wrappers; issuers that can pass through risk‑free yields without breaking par will dominate treasury use cases.

7) Settlement Interoperability: L2s and Chains as Neutral Netting Layers

- As supply grows, stablecoins act as the cross‑venue settlement asset across L2s/exchanges/custodians. Bridges and intent‑based routers become back‑office plumbing; end‑users see one USD balance abstracted across rails.

- Net effect: reduced need for bilateral credit lines between venues; more turnover can clear against shared dollar liquidity with atomic settlement and programmable delivery‑vs‑payment.

8) Risk and Regulatory Pressure: Collateral, Reserves, and Jurisdictional Arbitrage

- Scale attracts scrutiny: reserve composition, disclosure cadence, and bankruptcy remoteness become competitive features. Jurisdictions offering clear e‑money or stablecoin statutes will capture issuer domiciles and PSP partnerships.

- Basel/NSFR treatment for banks touching stablecoins will influence how aggressively they participate. Where bank capital charges are punitive, expect non‑bank trust structures and offshore issuance to grow, with front‑ends geofencing access.

9) Data Exhaust and Credit Scoring: New Primitives for Underwriting

- Rich, timestamped on‑chain cashflows (payroll in, supplier payments out, refund behavior) enable alternative underwriting for SMEs and consumers, especially in thin‑file markets. Stablecoin dominance standardizes the unit of account for these signals.

- Receivables can be tokenized and financed against real‑time payment data, compressing the cash conversion cycle for marketplaces.

10) Competitive Dynamics: Issuer Moats and Platform Power

- Scale begets utility: the more an issuer’s tokens are integrated across exchanges, PSPs, and banks, the more “acceptance network” effects kick in. This compounds via API distribution, compliance tooling, and fiat ramps.

- Multi‑brand UX will converge: wallets will abstract USDC/USDT/eURx balances behind a single “dollar” experience, but settlement venues will still prefer the most interoperable and transparent units, shifting volume toward issuers with best integrations and disclosures.

11) Crisis Behavior: Flight‑to‑Quality Within Stablecoins

- In stress, users don’t exit to bank deposits first - they rotate between stablecoins based on perceived reserve safety, chain reliability, and redemption throughput. Expect intra‑stablecoin spreads and rapid market‑share churn during shocks.

- For fintechs, this implies active treasury routing policies: holding multiple stablecoins, automated monitoring of peg deviations, and pre‑approved redemption channels.

12) Accounting and Reporting: Toward Real‑Time Attestation Norms

- As stablecoins become material operating cash, audit demands shift from monthly statements to continuous attestations and on‑chain proofs (reserves, liabilities, segregation). Vendors that offer programmatic proofs gain leverage with enterprise finance teams.

- ERP and reconciliation stacks will increasingly ingest on‑chain events natively, reducing manual break resolution and accelerating close.

13) Network Effects in Emerging Markets: Dollarization Without Banks

- Where local currency volatility is high, stablecoins function as de facto savings and pricing units. Fintechs that pair stablecoin custody with compliant cash‑out options become the new “neo‑dollar” banks, often with superior uptime and UX versus legacy rails.

- This increases policy tension: monetary authorities may tighten controls on off‑ramps or mandate licensed custodianship to manage capital flow visibility.

What to Watch Next (Leading Indicators)

- Share of on‑chain volumes settled in stablecoins vs. native assets across top L2s.

- Issuer reserve disclosures trending toward short‑duration T‑bills and intraday liquidity lines.

- Adoption of yield‑bearing cash wrappers by corporates, and accounting guidance from Big Four.

- Spread behavior between major stablecoins during market stress (peg micro‑deviations).

- PSPs and neobanks rolling out direct stablecoin acceptance and instant off‑ramps in key corridors.

All in all, the implications of such a stablecoin supply are much more than just crypto liquidity moves.

Businesses and fintechs should prepare accordingly to what is likely to come next, as this is only the beginning - as the supply increases, there will be even more adoption of stablecoins in our payments, services, and lives.

Read More:

VAULTs – What They Are, How They Work

Bitcoin in Your 401(k)? Deep Dive into the Trump Executive Order and Its Consequences

Pro-Crypto SEC Reform and Future Plans: A Deep Dive into the White House Crypto Report

Latest articles

Coinchange Financials, Inc.

261-250 University Avenue

Toronto, Ontario M5H 3E5 CANADA

Coinchange Financials Inc.

Corporation Trust Center 1209

Orange St.Wilmington,

DE 19801 USA

Coinchange Financials SP. Z.O.O.

Grzybowska 80/82/700

00-844 Warszawa, Poland

Note: Crypto assets are not legal tender, are not backed by the government, and crypto accounts held with Coinchange are not subject to FDIC or SIPC protections. The value of crypto assets are not static and can fluctuate substantially. Not all products and services are available in all geographic areas and are subject to Coinchange’s applicable terms and conditions. Eligibility for particular products and services is subject to final determination by Coinchange. Rates for our products are subject to change. Nothing on this website should be construed as a recommendation for any action. Coinchange is registered as a Money Services Business (MSB) number 31000304503627 with the US Financial Crimes Enforcement Network (FinCEN).